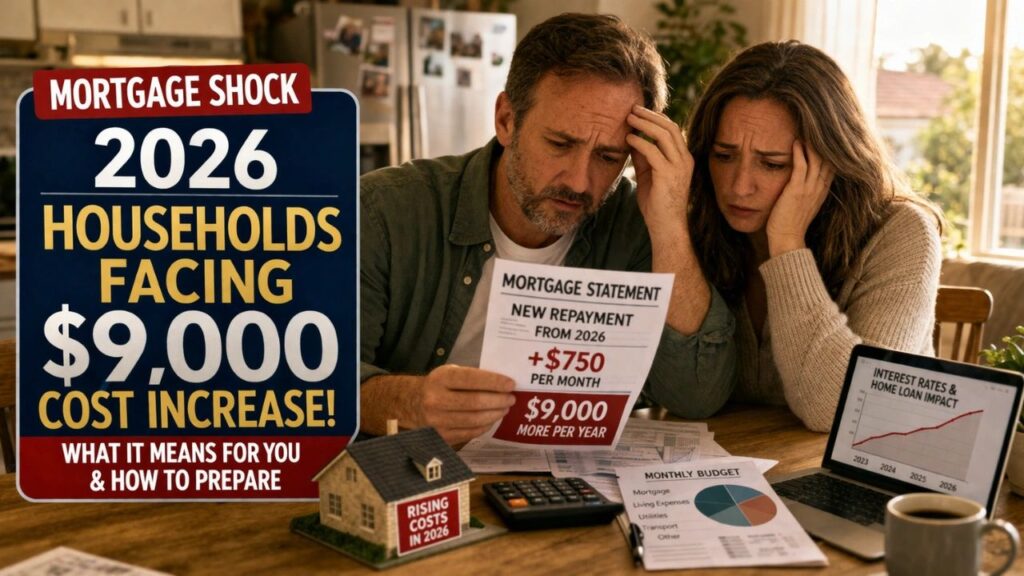

For many Australian homeowners, 2026 is unfolding as one of the most financially demanding periods in recent years. Mortgage repayments have risen sharply, and for some households, the increase amounts to as much as $9,000 more per year. This surge comes at a time when everyday expenses — from groceries to utilities — remain elevated, placing additional pressure on already stretched budgets.

The term “mortgage shock” has become widely used to describe this sudden jump in housing costs. It reflects the combined impact of rising interest rates, loan resets, and inflation-driven financial tightening. For families, investors, and first-time buyers alike, the reality of higher repayments is prompting careful reassessment of spending habits, savings strategies, and long-term financial planning.

Understanding the causes behind this shift — and what it means moving forward — is essential for navigating the challenges of the current lending environment.

What’s Driving Mortgage Costs Higher in 2026

Mortgage repayments rarely increase without clear economic triggers. In 2026, several interconnected factors have combined to create the sharp rise many borrowers are now experiencing.

Interest Rate Increases

One of the primary drivers of rising mortgage costs is the increase in interest rates over recent years. When rates climb, lenders pass on the higher borrowing costs to customers, resulting in larger monthly repayments.

For homeowners with variable-rate mortgages, this impact is immediate. Even a small percentage increase can significantly raise repayment obligations over time.

The Fixed-Rate Expiry Effect

During previous years of historically low interest rates, many borrowers secured fixed-rate loans to lock in predictable repayments. However, as these fixed-rate periods expire, borrowers are transitioning to variable rates that are considerably higher than before.

This transition — often called the “fixed-rate expiry cliff” — has created sudden payment increases for thousands of households across Australia.

Inflation and Lending Conditions

Persistent inflation has also played a key role. As inflation rises, central financial authorities typically adjust monetary policy to stabilize economic conditions. These adjustments often result in higher borrowing costs, which directly influence mortgage repayments.

Banks and lending institutions respond by recalculating lending rates to reflect changing market conditions.

Larger Loan Sizes

Another contributing factor is the size of modern mortgages. Property prices rose significantly in previous years, leading many buyers to take on larger loans. When interest rates increase, these larger loan balances amplify the financial impact.

The result is a higher repayment burden that can feel overwhelming, particularly for households with limited financial buffers.

How a $9,000 Annual Increase Happens

Understanding how mortgage costs rise helps clarify why the increase feels so dramatic for many households.

Consider a simplified scenario:

| Factor | Before Rate Increase | After Rate Increase |

|---|---|---|

| Average Mortgage Rate | Lower | Higher |

| Monthly Repayment | ~$2,500 | ~$3,250 |

| Annual Cost | ~$30,000 | ~$39,000 |

| Annual Increase | — | ~$9,000 |

This example illustrates how even moderate interest rate changes can lead to substantial annual cost differences. Because mortgages are long-term financial commitments, small percentage shifts accumulate quickly.

Who Is Most Affected by Mortgage Shock

While rising repayments impact many borrowers, certain groups are particularly vulnerable to sudden increases.

Recent Homebuyers

Those who purchased homes during periods of high property prices often hold larger loan balances. When interest rates increase, their repayment obligations grow more dramatically compared to smaller loans.

Variable-Rate Borrowers

Borrowers on variable-rate mortgages experience changes immediately when rates shift. Unlike fixed-rate loans, there is little protection from sudden repayment increases.

Fixed-Rate Borrowers Reaching Expiry

Households transitioning from fixed-rate loans to variable rates are among the most affected. The difference between previous and current rates can be substantial, creating a noticeable financial shock.

Low- and Middle-Income Households

Families with limited financial flexibility often feel the impact more strongly. Rising repayments reduce available funds for essentials, savings, and discretionary spending.

Property Investors

Investors holding multiple properties may face compounded repayment increases across several loans, increasing financial pressure.

Comparing Mortgage Conditions: Then vs Now

The difference between previous years and the 2026 lending environment highlights how dramatically conditions have shifted.

| Feature | Previous Years | 2026 Situation |

|---|---|---|

| Interest Rates | Historically low | Significantly higher |

| Monthly Repayments | Relatively stable | Increasing sharply |

| Household Financial Stress | Moderate | Elevated |

| Savings Capacity | Higher | Reduced |

These changes illustrate why many homeowners are reassessing their financial priorities and adjusting long-term strategies.

The Broader Impact on Household Finances

Mortgage increases rarely exist in isolation. Rising repayments affect multiple areas of daily financial life.

Households facing higher mortgage costs may experience:

- Reduced disposable income

- Limited ability to save for emergencies

- Delayed financial goals such as travel or education

- Increased reliance on credit facilities

- Greater pressure on household budgeting

Even modest repayment increases can disrupt carefully planned financial routines.

Warning Signs of Mortgage Stress

Recognizing early signs of financial pressure can help homeowners take action before problems escalate.

Common indicators include:

- Difficulty meeting monthly mortgage payments

- Growing reliance on credit cards or short-term loans

- Declining savings or emergency funds

- Delayed bill payments

- Reduced spending on non-essential items

Addressing these warning signs early can prevent long-term financial complications.

Practical Steps to Manage Rising Mortgage Costs

Although rising repayments can feel overwhelming, proactive financial management can reduce stress and improve outcomes.

Review Your Loan Terms

Understanding your current interest rate, repayment schedule, and remaining loan term is essential. Many borrowers benefit from revisiting their loan agreements to identify potential savings opportunities.

Consider Refinancing

Refinancing may provide access to more competitive interest rates. While not always suitable for every borrower, exploring alternative lending options can sometimes reduce monthly obligations.

Adjust Household Budgets

Reassessing spending priorities allows households to redirect funds toward essential financial commitments. Small reductions in discretionary expenses can add meaningful stability.

Build a Financial Buffer

Establishing emergency savings — even gradually — provides protection against unexpected financial pressures.

Communicate With Your Lender

If repayment challenges arise, contacting the lender early is critical. Many institutions offer temporary hardship arrangements designed to support borrowers during difficult periods.

What This Means for the Housing Market

Mortgage shocks do not only affect individual households — they also influence broader housing market conditions.

Potential impacts include:

- Reduced demand for property purchases

- Slower property price growth

- Increased caution among prospective buyers

- Greater financial scrutiny from lenders

- Changes in investment strategies

These shifts may reshape housing affordability trends in the years ahead.

Looking Ahead: Will Mortgage Pressure Ease?

Predicting future mortgage trends remains challenging, as outcomes depend on multiple economic factors.

Key influences include:

- Inflation trends

- Interest rate policy adjustments

- Employment and wage growth

- Housing supply levels

- Global economic conditions

While repayment pressure remains high in 2026, financial markets may gradually stabilize if inflation slows and lending conditions improve.

Q&A: Mortgage Shock 2026

1. What does the $9,000 mortgage increase refer to?

It represents the estimated additional annual repayment many households are experiencing in 2026.

2. Why are mortgage repayments rising?

Higher interest rates and loan resets are the primary causes.

3. Who is most affected by these increases?

Variable-rate borrowers and those transitioning from fixed-rate loans are among the most impacted.

4. Is the increase permanent?

Not necessarily. Future repayment levels depend on interest rate movements.

5. Can borrowers reduce repayments?

In some cases, refinancing or negotiating with lenders may help lower monthly costs.

6. What is a fixed-rate expiry?

It occurs when a loan’s fixed interest period ends and converts to a variable rate.

7. How much have rates increased overall?

The increase varies by lender but has been significant enough to impact many repayments.

8. Should homeowners consider refinancing?

It may be beneficial depending on available interest rates and associated fees.

9. Are assistance programs available?

Some support options may exist depending on eligibility and financial circumstances.

10. What should borrowers do if they cannot afford repayments?

Contacting the lender immediately is recommended to discuss hardship arrangements.

11. Will property prices change due to higher rates?

Higher borrowing costs can slow property demand and price growth.

12. How can households prepare financially?

Careful budgeting and planning for higher repayment levels can help reduce risk.

13. Are renters affected by mortgage increases?

Indirectly, as landlords may adjust rental prices to offset higher costs.

14. Is this trend limited to certain areas?

No, rising mortgage costs are affecting households across most regions.

15. Will interest rates decrease soon?

Future rate changes depend on inflation trends and broader economic conditions.